Greatly exaggerated death of the console

Your move, Sony.

We’re back to school (kind of) and starting with a string of high notes.

As we approach the release of the new consoles, we’ve finally found out what it’ll cost us and what it’ll offer. Carried by the momentum in gaming we saw in Q2 and Q3, this year’s finale looks to be a blowout. But what excites me most is the mounting counter-arguments against one narrative in particular: the Death of the Console.

For years now we’ve heard that the consoles are quickly becoming obsolete. They’re a dying device category that’s disrupted by glitzy tech firms that make smaller, shinier things. Right.

Sure enough there’s been hiccups in the past. Sony did price its PS3 too high back in 2006. And Microsoft shouldn’t have bundled the XOne with the Kinect. And it proved entirely impossible for Nintendo to immediately replicate the success of the Wii.

But here we are: despite the cancelations of every major event this year, the console makers have managed to still take center stage with their announcements and build up to a blowout year. Both Sony and Microsoft did an excellent job getting everyone excited about this allegedly obsolete technology, with hundreds of thousands of people watching simultaneously as they each laid out their release plans.

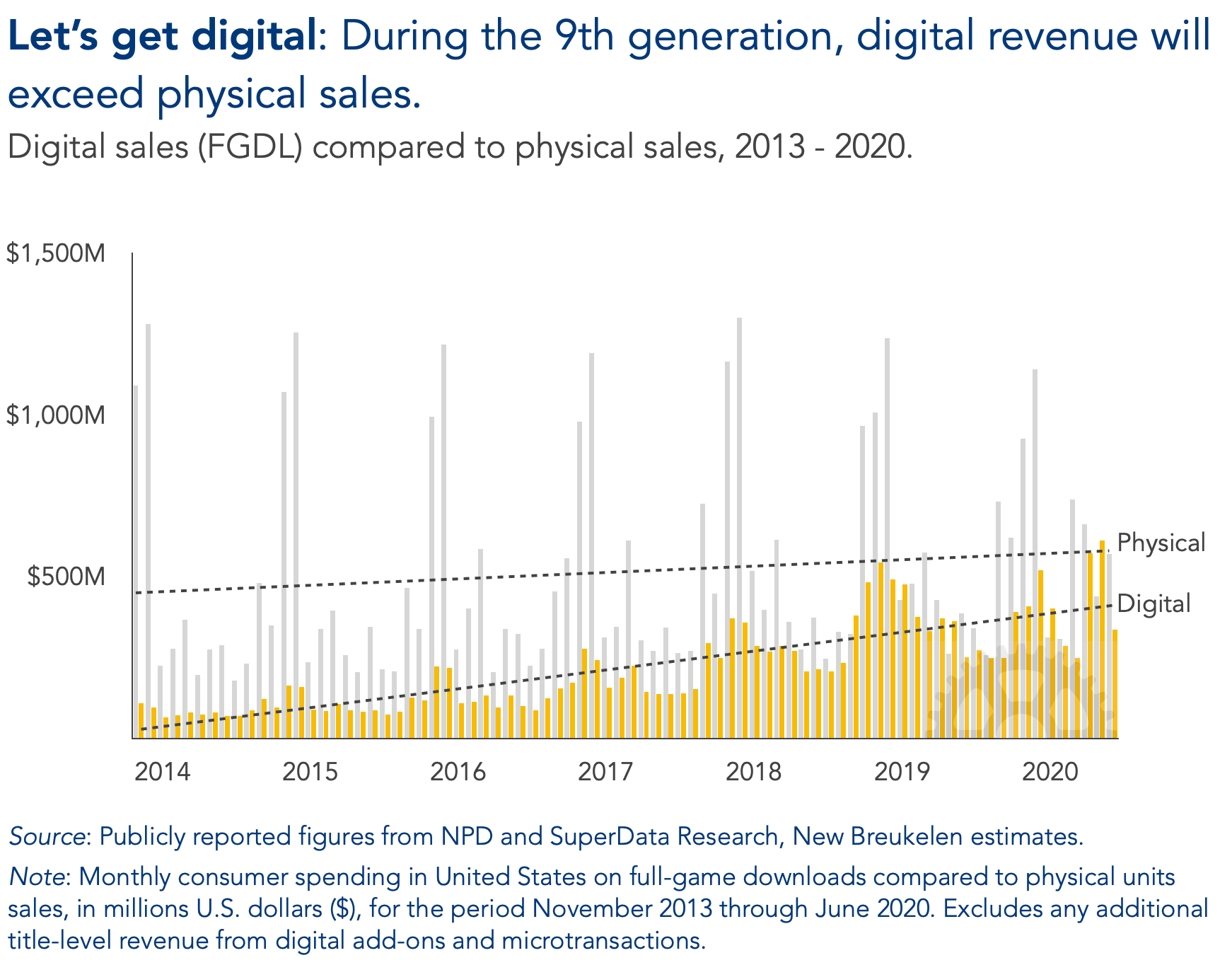

The world has changed. One explanation why the last generation was going to be the last is that neither publisher and consumers weren’t as keen yet on digital distribution. Downloading AAA content to a content with limited hard drive space is cumbersome. But despite the 92Gb download I had to suffer for Red Dead Redemption 2 and, worse, the 100Gb for Call of Duty Warzone, both publishers are doing just fine.

Console makers have finally figured out digital distribution. Their missteps along the way may have been evidence of some looming demise of the category, or it was a billion dollar process of trail and error as consumer behavior shifted. Looking at the past few years it seems obvious that digital revenue will outgrow physical sales.

Even so, physical distribution shouldn't be discounted just yet. There are large areas where consumers cannot download anything at a reasonable rate or where there's a distinct preference for physical discs. Japan, for instance, has historically been really slow in moving towards digitalization. I doubt, however, that it will save GameStop, which stated during its recent earnings call that it could bring physical discs to consumers faster than digital downloads.

Consoles aren’t just devices. It is shortsighted to consider consoles mere boxes to be sold at volume and therefore perpetually at risk of being out-invented. Technological disruption of the kind that Apple has shown us applies to competing with archaic systems that fail to leverage platform dynamics. Value chain optimization is a product-based business. However, the resilience of gaming consoles comes from the fact that they’re carefully cultivated ecosystems that manage to evolve over time.

Consoles are more alive than ever.

On to this week’s update.

NEWS

Microsoft’s $7.5bn acquisition of Zenimax

It’s one way to start the week. Beyond the size of the acquisition, which is roughly three times more than what it paid for Minecraft and Nadella’s first big purchase as CEO, it tells you that Xbox is now fully prepared for the escalating platform wars, whether that’s on console, PC, or in the cloud. It also raises the barrier to entry for aspiring new contenders like Amazon and Google. (More on this in a moment.)

Strategically it is a decision consistent with Xbox’ push behind its GamePass subscription. It goes without saying that having a strong library of games to sway people to sign up is key. Building IP from scratch is expensive and time-consuming. This purchase instantly increases the value of the service. Microsoft is clearly serious about its long-term success and has hereby made a commitment to the overall gaming ecosystem. That is more than you could say for some other platform holders who only invest piecemeal amounts and mostly focus on extracting rent.

The price tag seems high, but that’s relative. Microsoft is currently trading at $200/share, which is a +46% increase since the low point in March, and money is cheap right now. Buying real estate is always pricey and will give it a better return on its money than holding onto cash, especially at a market cap of $1.5 trillion and interest rates at zero.

Next, it is clear that Xbox no longer sees PlayStation as a mortal enemy. An acquisition of this size affords Microsoft to go where no competitor can follow: a platform agnostic future. Sony is of course trying to cross-over, but it does so at a disadvantage. It has twice the install base as the Xbox and I’m sure that the 9th generation will be similar. But it has a much more modest share of the combined PC, console, mobile and, soon, cloud universe. Most likely we’ll start seeing Sony porting its top-tier IP to other platforms to broaden its reach.

The timing of the announcement further suggests that Microsoft deliberately waited for the Sony announcement of the PlayStation’s pricing. Having traditionally outmaneuvered Microsoft with better IP, Sony now finds itself more equally matched as Xbox is closing the content gap. Nevertheless, this acquisition won't really be meaningful for Microsoft until next year, but it promises enormous potential in terms of hosting modded content. As the industry moves into user-generated content, that may prove to be a key differentiator.

Finally, it has the potential to affect the industry’s landscape as we move into the next gen. We already knew that all major platforms have been looking to buy exclusive content. This has increased the valuations of the slowly dwindling number of content creators. By taking Zenimax off the market, it means there are only a few remaining potential acquisition targets, and these will come at a high price. For Google and Amazon to successfully breach the games industry and become a notable competitor to the incumbents, they have few other options available than buying EA, Activision Blizzard, Take-Two, or Ubisoft. The latter here is the most likely one to go first because of its relatively modest market cap of ~$10bn. But beyond that, Big Tech is going to have to shell out a lot of money to get this done. Most likely Amazon will choose to take a role as a distributor rather than a full platform by opening a digital storefront. Google may have a lot of viewers on YouTube but is going to find it prohibitively expensive to buy a legacy publisher.

If nothing else, now Phil and Todd can now get a group discount at whatever leather store they both buy their jackets. Link

Apple’s new content bundle

There's a saying in business that you can create value in two ways: bundling and unbundling. It is no surprise that Apple has clearly chosen the former. It tells us three things: first, Apple is unrelentingly moving forward with its drive towards higher services revenue as part of its overall earnings. It makes income more predictable and therefore appreciates its share price because it mitigates Apple's exposure to hit-driven economics in its device business. Wall street adores recurrent revenue.

Second, after firing a shot across the bow with Epic which was clearly meant to let the game maker and anyone else with ambitions to go rogue know that it is the boss. Do not defy the king's rule that governs the App Store. With Apple One, the firm is competing more directly with every other content subscription out there. Do I need Apple News? No. Will I occasionally look at it if it's part of a bundle? Maybe. Will it prevent me from subscribing to, say, another news service? Probably.

Third is the observation that Apple's individual subscriptions weren't performing as well as it had planned. This should come as no surprise given the firm's demonstrable disdain for content providers in any category. Apple would rather just bundle all of it and create a type of multi-headed hydra to scare music, video, news, and game companies. But it also tells you that its own content efforts haven't gone so well.

Here’s the most important question: Does that matter? Does Apple care if its services do well? The answer is no. Because of ‘cross-market recoupment’ Apple is in a position to subsidize the cost of its offering in one market (content) with high profit margins in another (smartphones, tablets). As far as Apple is concerned, its services could be free if it meant that it would sell more iPhones and at higher margins. That’s different from the more conventional platform economics we find in gaming where Microsoft/Sony/Nintendo invest in a hardware platform at a loss and recoup it by selling lots of software. However, in the latter case the interests of platform holders are aligned with content creators. In Apple’s case, it is irrelevant to them what happens with content creators, even if those are large and wildly popular. Think different, you know.

As a bonus, the inclusion of Fitness+ indicates that Apple has bigger plans in the fitness category. I would not be surprised to see it use its vast coffers to acquire an in-home fitness firm like Peloton. Link

Live streaming’s coming of age

It would have been nice, of course, if live streaming had been a ready-made industry. But as all new business models, there are a lot of growing pains. Here’s an excellent overview by Cecilia D’Anastasio on the volatility and fallout of the live streaming business. It should need no explanation that this segment has become critical to the marketing of titles. But its current level of immaturity presents a whole new risk profile. Link

Nintendo discontinues the 3DS

Of course the Switch is a superior device in many ways. But it has yet to enter whatever part of my lizard brain dispenses that nostalgia hormone. The fliptop was a perfect throwback design aspect that made this a textbook example of a time machine. Thanks you for everything. Link

BTS readies itself for its Fortnite premiere

The popular boy band will drop a new song in the Fortnite multiverse. It's now part of the standard playbook for musicians and artists to make an appearance here as well in addition to more conventional promotional effort. I'm excited for you. Link

Unity IPO pops

Initially valued at $11bn, Unity had a great day one at $13.6bn and a high of $76.79 per share. Having seen the trajectory from when Riccitiello first took the helm to today, it’s an impressive and a deservedly warm welcome. Link

MONEY, MONEY, NUMBERS

An impressive list of top-tier publishers lined up to give Bunch $20MM for its series A. The list includes Electronic Arts, Take-Two, Krafton, Ubisoft, Mixi, Miniclip, Colopl, Riot Games, Ubisoft, and Supercell. Dang.

Embracer group acquired Vertigo Games for $59MM to make VR games. Link

Finnish game maker Metacore received $17.7MM in funding from mobile gaming giant Supercell.

Esports data firm Bayes raised $6MM from Pohlad Family investment group, Fertitta Capital, and the Sony Innovation Fund.

Gameloft acquired The Other Guys for an undisclosed amount to diversify.

Stillfront acquired Nanobit for up to $148MM.