Three decades of games industry consolidation

Will Microsoft suffer the wrath of Khan?

This must have been the longest January of my life.

The pandemic had already robbed me of any sense of day or time. But then, on the final day of the month, Sony announces its $3.6 billion acquisition of Bungie. Talk about getting snowed in. It has left me reduced to orienting myself by calendar months only.

Thank God it’s February (TGIF).

Anyway, this week’s announcement is a continuation of Sony’s strategy that rhymes with its acquisitions and investments elsewhere, including its purchase of Insomniac Games for $229 million in 2019, buying a $400 million stake in Chinese live streaming service Bilibili in 2020, making a $200 million investment in Epic Games last April, acquiring Crunchyroll in August 2021 for $1.2 billion, and, finally taking minority stakes in Discord, Scopely, and Devolver Digital. Phew. As a consumer electronics firm, Sony has an extensive history of buying its way into entertainment markets like video and music to encourage you to buy their TV sets and audio equipment.

What doesn’t get discussed much is the imminent shortage of talent in the industry. Headlines cover the IP and valuations, but humans are arguably an equally important component. The industry has grown four-fold but it takes time to become a seasoned dev. I did a talk at a recent conference in cooperation with the German government which wanted to know how to reduce the backlog in talent. Abundant venture money has convinced more than a few mid-level managers that now is the time to pursue that dream of running their own studio. And all that crypto mickey mouse money is fueling FOMO to the moon while creativity remains firmly on the ground. The games industry is increasingly cash-rich and talent-poor.

Sony has already stated Bungie will continue to operate on all platforms, etc. That tells you that they’ll use the team to bring other Sony properties online. After being the last holdout with cross-play on Fortnite, Sony must have realized they need to beef up their internal capabilities, especially since they cannot compete with Microsoft on infrastructure and cloud services. That’s where Bungie can play a meaningful role.

I’m not wagering any credentials here when I say that consolidation is going to be a big theme this year (more below). What’s different, however, is that we’ll be looking at game acquisitions that bleed into other categories. Especially Big Tech is going to be upgrading from perusing to purchasing. Netflix's share price cratered 37% in January. It will therefore be looking to broaden its exposure to growth categories like gaming to regain momentum.

And to consummate its promise to the metaverse, Meta is going to need a notable acquisition. Something saucy. Like the corporate equivalent of a red convertible. I’m thinking OpenSea or another Web 3 marketplace where it can build some kind of eBay-for-NFTs-but-owned-by-formerly-Facebook hub.

Finally, I’m happy to report that crypto-winter coincides with several inches of snow here in Brooklyn. It allows for some good old-fashioned, non-fungible sledding with the 8-year old. I’ll see you at the bottom.

On to this week’s update.

BIG READ: Analyzing 30 years of consolidation in video games

With three record acquisitions in the games industry in the starting weeks of January, the tone is set for 2022.

First, Take-Two acquired Zynga for $13 billion to expand its footprint in mobile and to gain access to a more casual audience. And, maybe CEO Zelnick is assembling a springboard into media mogul-dom. Next, Microsoft acquired Activision Blizzard for $69 billion to bolster its digital service offerings like xCloud and Game Pass and instantly redefined the boundaries of the global games market. Someone should check in on Stadia and Luna, provided they still live at the same address. And, as for Sony, it has been on an acquisition spree to bolster its digital offering and compete with Microsoft’s Game Pass service.

According to its most recent earnings, PlayStation relies on services for two-thirds of its income. Accordingly, the Bungie acquisition sets the company up for a strong offering when it launches its revamped gaming subscription in March, and insulates it from current supply chain issues that have made it virtually impossible for average consumers to get their hands on a PS5.

Earlier in my career, I spent most of a decade gathering data and analyzing ownership trends in media and entertainment industries. In fact, I still am, as a co-applicant for the Global Media and Internet Concentration Project. So whenever big mergers take place, I get really excited.

It is also no secret that I’m swooning over the appointment of Lina Khan as chair to the FTC. Her work on reframing antitrust policy in the context of digital platforms is brilliant, for one. Historically, much of the conversation around media concentration focuses on Rupert Murdoch-type moguls that accumulate a variety of media outlets, limit consumer choice, and drive up prices. Economies of scale are a common media strategy, of course, and much of the current media landscape is pretty clumpy.

Khan’s work focuses on more contemporary issues. Specifically, she seeks to tackle the challenge of how to appropriately regulate multi-sided platforms (e.g., Amazon) that can give away services in a content market (e.g., video) by subsidizing it with increased prices elsewhere (e.g., online retail). Anyway, her recent hiring of a former colleague, Olivier Sylvain, tells me she means business. Big tech beware.

Innovation through acquisition

So, how, exactly, does the string of mergers impact the games industry? Elsewhere I’ve already laid out the reasoning why Microsoft would shell out $69 billion, and what Take-Two is planning. But what are the implications of all this consolidation?

The short answer is that consolidation threatens innovation. And that claim, at least in the video games industry, has merit.

According to a 2017 study by my buddy Joost Rietveld and his colleague Masakazu Ishihara, acquisitions have a two-fold effect. On the one hand, product quality improves. When a publisher acquires a studio, the most common justification is the target studio’s ability to execute. Combined with the deeper pockets and stronger ties to industry reviewers and tastemakers of the new parent company, their output receives more favorable ratings. In turn, this has a positive impact on sales. Large publishers are capable of pushing content to the foreground, expanding visibility, and selling more.

On the other hand, innovation suffers. Buying another company often serves as a replacement for internal innovation. According to Rietveld and Ishihara, indies release more novel intellectual property than acquired studios. Independent creatives can and generally do take more risks. Conversely, acquired companies are less likely to release innovative video games.

So does that mean we should be worried considering the size of the acquisitions?

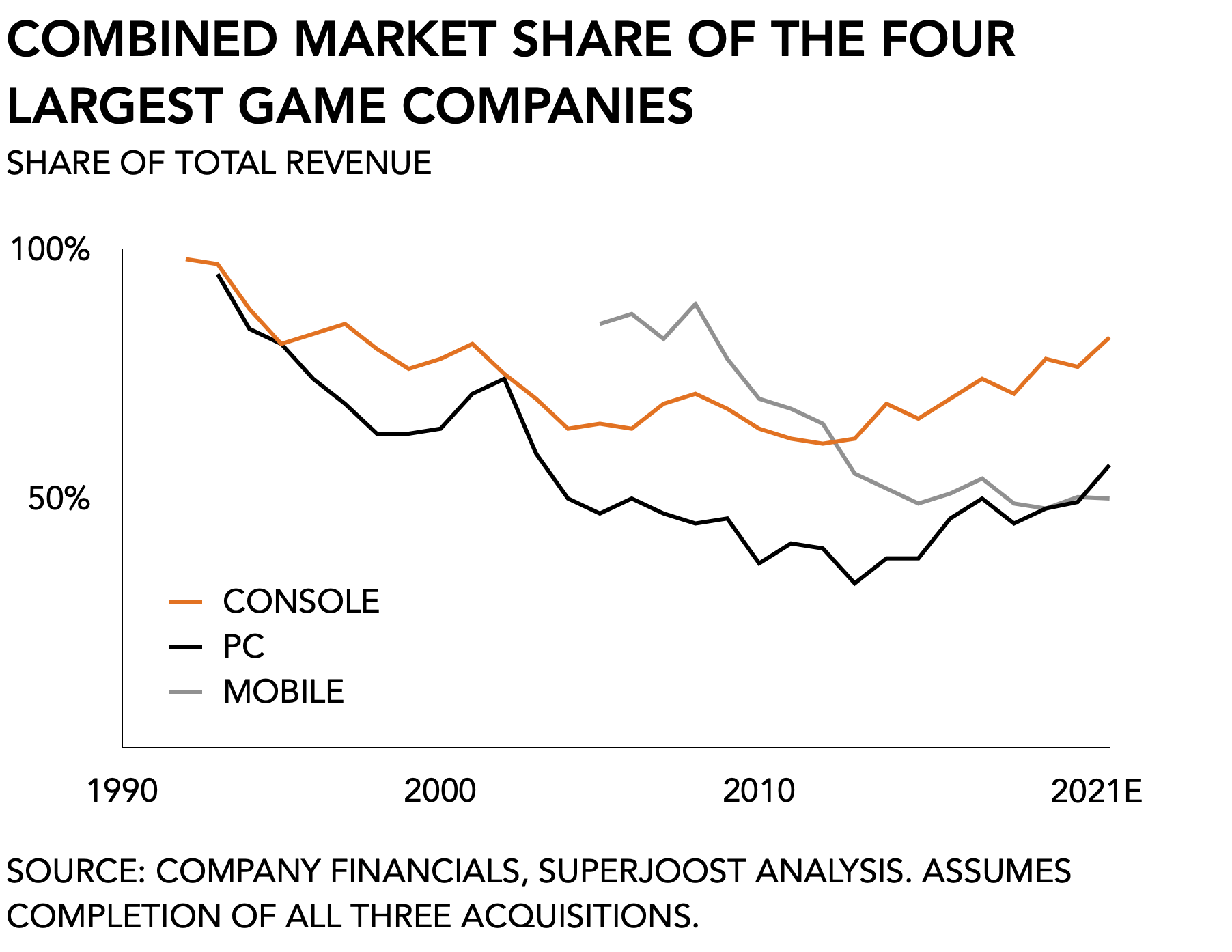

Well, here’s what the data says about the degree of concentration in the games industry. The following builds on 30 years of market data collected across both privately-held and publicly-traded game companies. It is, in effect, a continuation of the work I did for my book One Up, which discusses concentration and consolidation trends in the games industry in greater detail (chapter 8). For my purposes here, I assumed the completion of all three proposed mergers and calculated market shares based on what is currently available (Microsoft already reported its 2021 revenue, for example, but others did not). It’s the first draft.

After a period of declining concentration on all three platforms, both PC and console markets are showing an increase in the total market share held by the largest four firms in their respective categories. For 2021E, the top four companies in console control an estimated 82 percent of the market; for PC that number is 57 percent, and for mobile 50 percent. The distinct U-shape indicates an increase in market concentration in recent years.

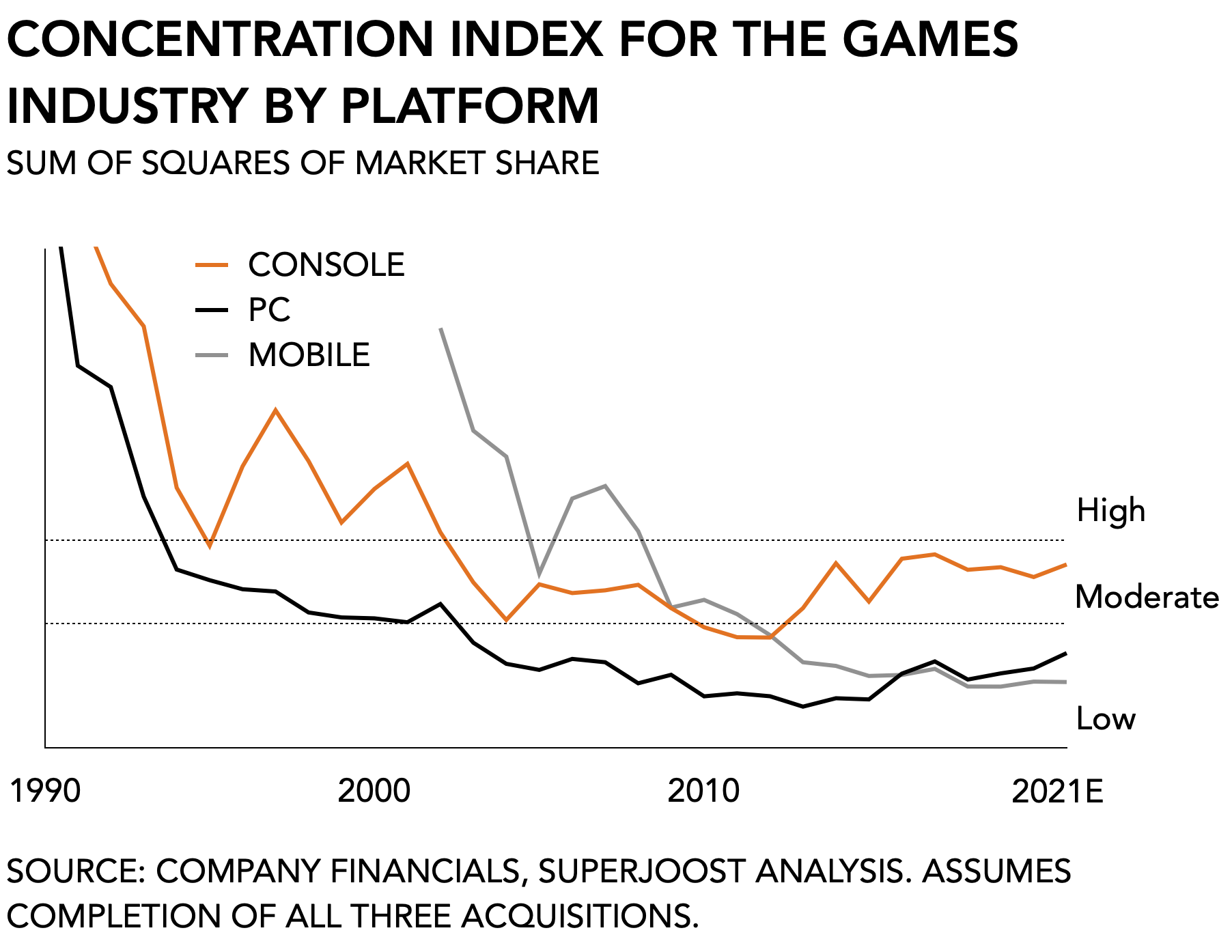

Looking only at the four largest firms doesn’t tell us anything about the relative size of the participating companies. For that reason, the Department of Justice uses something called the Herfindahl-Hirschman Index, which calculates concentration by squaring the market share of each firm competing in the market and then summing the resulting numbers. For the video games industry, we get the following numbers.

Since 2010 when all three categories were considered unconcentrated by the standards of the DoJ, there has been a notable increase in consolidation in the console market. Both PC and mobile have stayed well below the threshold and remain unconcentrated. In 2021E the HHI for the console business reaches an estimated 2,207 and is up considerably from its low of 1,328 in 2012.

Succinctly, the MSFT/ATVI acquisition really only endangers the console business. It is important to note that Zynga, which is largely a mobile game company, doesn’t share any overlap with Take-Two, which focuses on PC and console. Similarly, Bungie contributes only marginally to Sony’s market share, which is absent from mobile and only just starting to take root in PC. That leaves the MSFT/AVTI merger. Based on the data I’ve collected so far, the acquisition of Activision Blizzard only impacts the console market as evidenced by a pronounced U-shape for its overall concentration trend.

That’s not super-surprising. The games industry is hit-driven, for one. That makes it difficult for even the largest and wealthiest firms to maintain an iron grip on the market, even if they have abundant capital. Moreover, consumer spending on interactive entertainment as a whole has grown so quickly in recent years, even before the pandemic, that it is virtually impossible for a single firm to claim control over the market. Tencent, the world’s largest publisher today, barely made a billion dollars a decade ago. The combined globalization of gaming and the popularization of mobile has allowed the industry to quadruple in size, which makes it difficult for anyone to monopolize it.

The wrath of Khan

The data tells us two things. First, despite the expectation of scrutiny, the FTC will probably leave the MSFT/ATVI merger alone. Even as concentration increases, the overall trend is relatively muted by the fact that the industry as a whole continues to grow, too. Concentration is higher, yes, but the spectacular growth of the overall games industry and its sub-segments mitigates any one firm’s ability to claim it for themselves. Consolidation has not reached the point yet where it, historically speaking, warrant the intervention from regulators, although that may change if, for example, its current momentum start to subside.

Furthermore, a platform buying a publisher is what is known as a vertical merger as two different value chain participants now operate under the same flag. Generally speaking, regulators are more worried about horizontal mergers. For instance, the much-publicized proposed acquisition of Arm by NVIDIA falls in this category. It was predictably scrutinized by UK regulators and NVIDIA has started to quietly abandon the whole idea.

Had Microsoft acquired Nintendo, which by the way currently has a market cap of $57 billion (!), or even Sony ($132 billion) it would severely reduce consumer choice and, by implication, allow Microsoft to raise prices. That, too, makes no sense. Microsoft has been pushing a strategy that focuses on the largest possible addressable audience, diversity, and financially accessible hardware and services.

Second, much of the debate around concentration in media and entertainment has to do with access to information in the context of democratic discourse. The underlying reasoning to regulate, for example, how many radio stations any one firm can own in a single market has to do with access to a broader set of ideas. Video games, remarkably, are generally not considered to contribute to the greater civic conversation.

In my opinion, games are excellent at conveying and negotiating a broad range of novel ideas. But beyond violence and gambling, most politicians don’t really care to look. Hell, even the largest firms in games themselves are disinterested. Hollywood and the music industry have maintained clear stances on their shared belief systems and the vocalization of those that need to be heard. Meanwhile, game execs struggle with the realization that for the words they chisel into their buildings to carry meaning, they must enact them in practice but don’t. As such it is most likely that after a stern conversation around access to content and consumer choice, regulators will simply move on from recent mergers.

As a final observation, consolidation tends to occur whenever the next generation of consumer technology draws near. Large organizations insulate themselves from imminent volatility by expanding their content catalogs. The push into cloud gaming and its subscription-based revenue model would certainly qualify as such a shift. Twenty years ago few felt there was room in the industry for a third console. Many ignored PC gaming for years. And mobile was an after-thought. If I had to guess, the current ebbing precedes a massive wave that will flood the market with abundant content for consumers and opportunities for creatives that will wash away any false sense of scarcity.

NEWS

Team Zuckerberg renames its VR goggles

No mid-life crisis is complete without a full, catastrophic rebranding of things that didn’t need fixing. Dropping the Oculus name is poorly timed, for one. The device just started to hit a stride, selling an estimated 7 million units last year.

Admittedly, the experience is improving. I’ve been experimenting with its different applications which are well ahead of its predecessors from even a year or two ago. The abundance of 360-degree footage on YouTube also helps. Watching Netflix as if I’m in some comfy chalet is fun, yes, but it’s not a need-to-have. Many of the social experiences remain scattered and incoherent. And, in case you were wondering, the narrow ranges in cinematography and demographic diversity make VR porn largely a snoozefest.

In the absence of a clearly defined killer app, the goggles formerly known as Oculus continue to look for relevance. Moreover, it is a largely decontextualized experience. The console’s success, for example, depended on its ability to become the center of the living room. Mobile gaming takes place while you’re doing other things. PC gaming is a celebration of your newly built rig. But VR is only about VR. That’s not meta. It’s mediocre.

Epic Game Store grows as planned

Team Sweeney released a bunch of numbers on the success of its digital storefront. As part of a broader crusade against platform holders everywhere (e.g., Apple, Valve), PC gaming is a critical frontline. The firm has made several notable acquisitions to give its storefront a more fleshed-out personality beyond just Fortnite and, in honesty, their emphasis on colorful goofy multiplayer fun cleverly positions it somewhere between Nintendo and everyone else.

It’s important to remember, however, that much of the current traction and success are the direct results of Epic’s aggressive spending. In establishing a new platform, the combination of subsidizing third-party content creators and releasing exclusive titles is critical. With 194 million PC customers (presumably that means spenders), 62 million month actives in December, and a combined total of $840 million in revenue, the Epic Game Store is doing well. Team Sweeney is giving away a lot of value to attract players: a total of 89 games valued at $2,120. Paid for by Fortnite players, I’m guessing.

As it continues to build on its success, it will predictably run into the same problems that have shaped policies at rivals like Apple, as Epic’s interests shift from catering to third-party content creators to maintaining its borders. It leaves us the question of whether Epic will become the maverick firm in the video game industrial complex, or just part of the overlord upper class.

PLAY/PASS

Pass. Here’s a glaring oversight in the VR adaptation for Resident Evil 4 resulting in “tit-punches”. Welcome to the future of entertainment.

Play. Now that the NY Times has purchased Wordle, go read this analysis “Deep Wordle” and step up your game. The Sunday crossword is about to meet its match.