AI is making everything more expensive

Hardware costs, business risk, and career uncertainty are all rising.

The most important resource in gaming is talent, not tech.

Late last week, two of the world’s largest companies in the games industry, Xbox and Apple, announced price increases. What had remained mostly a problem for die-hard gamers who invest in expensive hardware to customize and maximize their experience has now started to bleed into the broader consumer electronics market.

The immediate pain is felt across the entire value chain. For one, as chipset manufacturers embrace what they call their “post-consumer” future, consumers are getting priced out of hardware.

In an exquisite investigation titled ‘Collapse of Personal Computing,’ the YouTube channel Gamers Nexus released a three-and-a-half-hour-long video with interviews and reflections on how the cost of chipsets is impacting the custom PC and peripheral market.

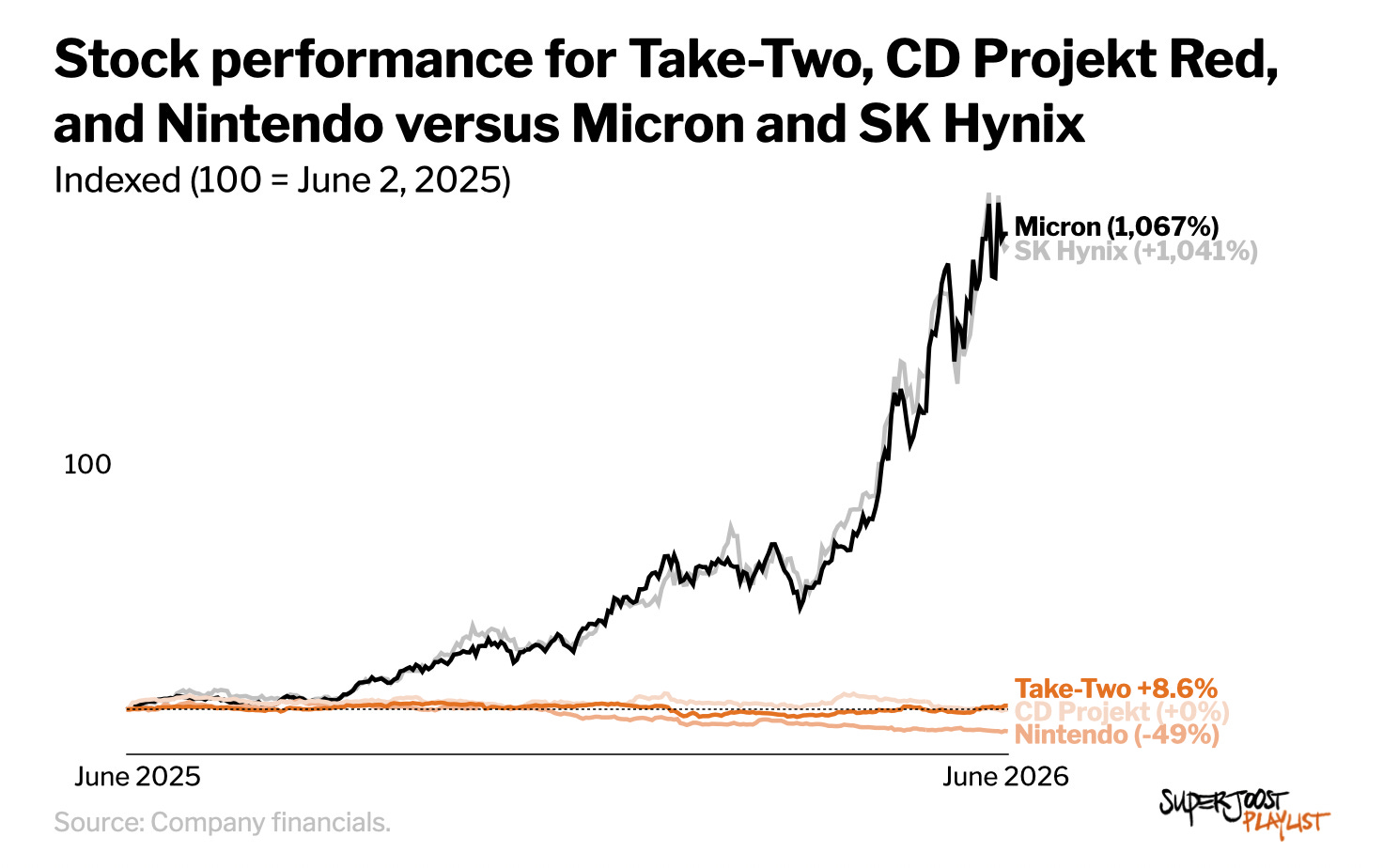

The magnitude is hard to overstate. Corsair’s Director of Marketing, George Makris, a three-decade veteran of the components trade, points out that memory has always been volatile, but on a normal day, that means a swing of 10 percent in either direction. What the market is living through now is something else: “up 400% is not typical.” To put a price on it, a 32GB memory kit that sold for roughly $120 a year ago now commands a multiple of that, when it is in stock at all. As a result, the companies making the memory are up tenfold since last June, while the ones making games are flat or down.

AI data centers are now directly competing with consumers for access to hardware components, driving up gaming hardware prices. The same dynamic that put 2026 World Cup tickets out of reach for regular fans is now coming for PCs. Gartner predicts this could entirely eliminate the sub-$500 PC market by 2028, shutting out the lowest-income consumers.

Rather than buying hardware, people will rent access to computational power and access to applications in the cloud. For consumer markets like the US, where people historically buy and own their device (e.g., PC, console), the notion of owning nothing and logging in on a stock machine at some public place seems odd. It is common for billions around the world, though, few of whom grew up in a world where hardware ownership was a thing.

A second pain point is the increased risk profile for publishers.

The broader lack of investor understanding of how games are actually made is compounding that exposure. In late January, the announcement of Google’s Project Genie, a prompt-based AI solution that generates explorable 3D environments, triggered the sell-off of several prominent game makers’ shares.

Publishers found themselves having to explain to their investors that, no, a simple prompt would not produce a one-to-one experience comparable to what has traditionally taken years to accomplish. Take-Two CEO Strauss Zelnick adamantly denied that AI would easily replace them. Nevertheless, share prices took months to recover as investors remained skeptical. A single product demo from Google reset the risk profile and long-term expectations of publicly traded game makers.

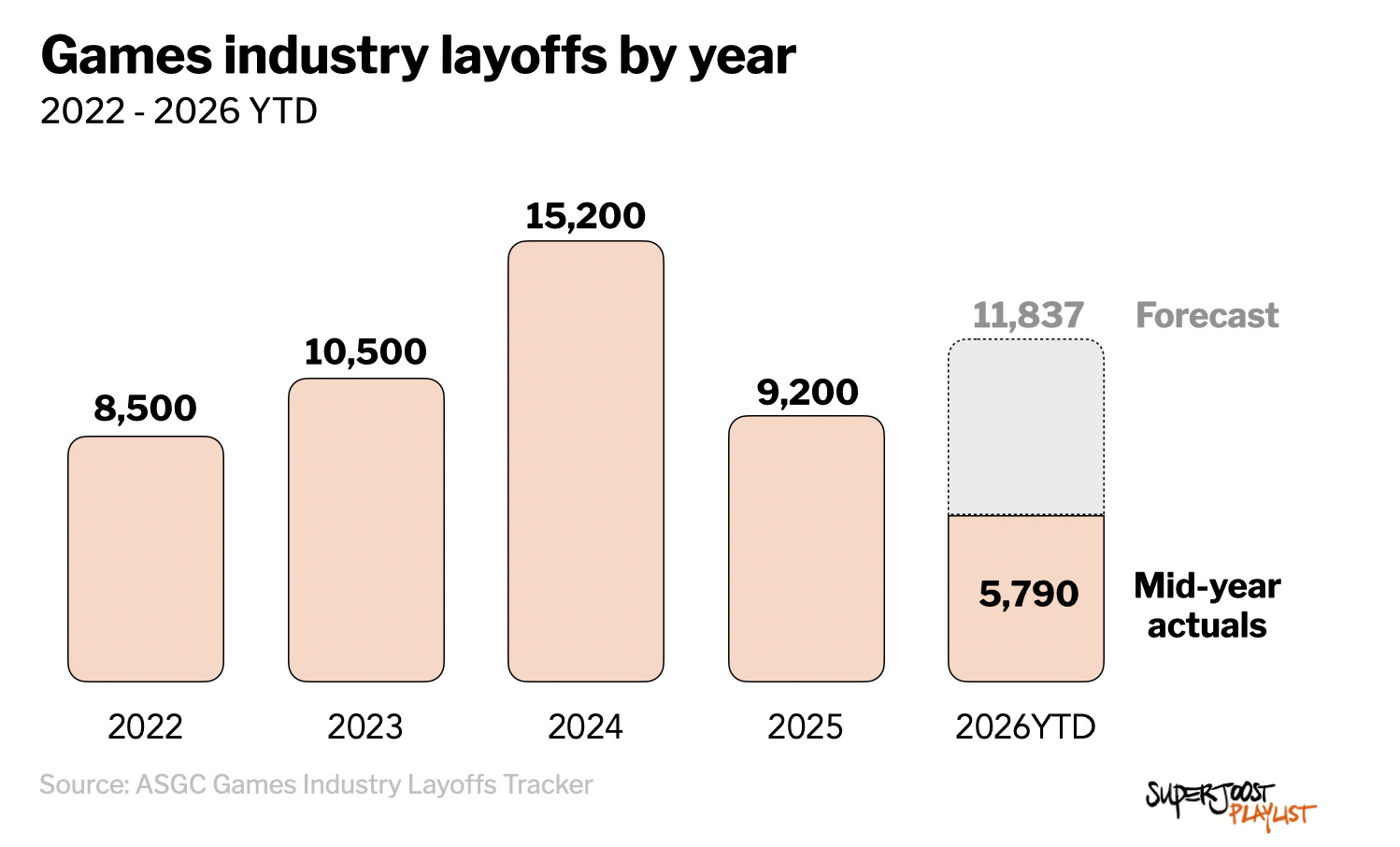

And finally, the same pressure is hollowing out the workforce. The resulting layoffs have a nasty knock-on effect: they discourage creatives.

Pure-play game makers have reduced their overall headcount by 7.2 percent from 2022 to 2025. Well-established firms like Ubisoft, Square Enix, and Perfect World have laid off thousands of employees, and among the largest companies, such as Xbox and Sony, many more layoffs are expected.

Eventually, such cuts hit the bone.

Rather than providing the infrastructure and organizational stability necessary for long-term creative work, a fealty to financial cycles and increasingly powerful tech overlords marginalizes talent. What is the upside of joining a big publisher to learn the ropes and start your career? Companies’ incentive to replace low-skilled labor with tech solutions removes an already precarious on-ramp for incoming talent. Sure enough, that looks clever in a quarterly earnings report as investors look for margin growth, but systematically reducing headcount in response to external volatility is a short-term solution. Making games is hard, costly, and time-consuming. If you’re not investing in talent and cultivating their ability to develop great experiences, are you even a games company?

This is where the Play Pendulum starts to swing. When content becomes more expensive to create and maintain, innovation rarely comes from spending more money. It comes from finding new ways to reach audiences, distribute experiences, and build communities.

Historically, however, game makers are remarkably resilient. Contrary to technological innovation, which is so often institutionalized from the top down, creative firms invent new ways to build and distribute games. By finding new approaches to existing problems, firms such as Id Software, Valve, Nexon, Riot Games, Supercell, and CD Projekt outperformed their peers. What set them apart was not technology but a refusal to stop investing in the people who make the games.

Winners versus losers

The dividing line between winners and losers is organizational, not just financial.

The most vulnerable firms are those whose leadership cannot prioritize long-term creative output over short-term financial expectations. That pressure is not exclusive to public companies, but public companies feel it most acutely.

In the wake of the pandemic, publicly traded firms in particular have focused on economies of scale. Fueled by cheap capital, they sought to mitigate their exposure to an impending decline by increasing size, ultimately resulting in an industry-wide trend toward consolidation.

That mandate shifted toward showing revenue growth and, by extension, margin growth. Shareholders valued firms that proved capable of earning more while using fewer resources (read: human capital). The strategy worked until it didn’t. Now, many of them find themselves trapped in a death spiral, forced to cut jobs and issue buybacks to prop up the share price, while forsaking innovation and long-term investment.

When a big publisher can't offer financial stability, it becomes more appealing for developers to assume all the risk themselves and see their creative vision come to life on their own terms.

A few outliers prove the point: both Take-Two and Nintendo are public, yet both provide aircover for developers to ensure the eventual launch of a title is a success. We've been waiting for GTA6 for almost 13 years now, and at its June shareholder meeting, Nintendo told investors it has raised employee base salaries by 10 percent even as the rest of the industry cuts. These firms manage some of the most successful franchises in the industry, and they resist that pressure for a simple reason: their primary customers are not investors. They are players.

The winners in the current market environment are firms with organizational flexibility, many of which are privately held. That flexibility lets them navigate financial pressure, from the big independents like Epic Games and Valve, which can operate as they see fit, to smaller and mid-sized studios.

In an earlier analysis, I showed that privately held firms were growing their headcount while their publicly traded counterparts were downsizing. Their ability to accept lower margins is proving to be a competitive advantage. Moreover, when it comes to thinking creatively about how to reach audiences and build a sustained relationship between players and their games, this category of game makers currently has the upper hand.

AI is making everything more expensive, and, in response, gamers and game makers will turn to new ways to play and make games. This is the Play Pendulum at work. But instead of providing efficiencies and empowering creatives, AI is catalyzing the current push into distribution innovation.

We’ll see it in the platforms that are doubling down on user-generated content and creator economies. Epic is the clearest case: the same company that is folding Fortnite's creator tools into its next engine and is pushing cross-game, portable content is betting that the next decade of growth comes from distribution, not from bigger production budgets.

The industry has swung this way before.

Free-to-play, the app store, the creator platform: none of these were tech-first innovations. They arrived when creatives, under financial pressure, reinvented their business models. It suggests that firms cutting talent today will soon fall behind, both short-staffed and short-sighted.

NEXT UP

To recover from the Dutch team’s elimination from the World Cup, I’m headed up the mountain for a few weeks, where I will yell at the moon. And do some writing. ❤️⚽️