Platform politics

Gatekeepers change position to meet culture shift

The SuperJoost Playlist is a weekly take on gaming, tech, and entertainment by business professor and author, Joost van Dreunen.

It’s only week two of the new year but I already know what I want in my stocking in December. It’s the new Sony PlayStation AFEELA. It costs $90,000 and comes with four seats, cupholders, and a built-in steering wheel.

On to this week’s update.

BIG READ: Platform politics

The transition into the new year marks a pivotal shift in digital platform governance.

This week Meta CEO, Mark Zuckerberg, announced that the firm is getting rid of fact-checkers. The announcement tells you everything you need to know about how tech companies are recalibrating their positions within an evolving political landscape.

Meta announced sweeping changes to its content moderation policies in what appears to be a strategic pivot to appease Donald Trump and the Republican party. The company is dismantling key safeguards it built after 2016, including ending its fact-checking program, relaxing restrictions on previously prohibited speech targeting marginalized groups, and dramatically reducing automated content filtering.

According to Zuckerberg,

“Fact-checkers have been too politically biased and have destroyed more trust than they’ve created.”

I’m sure it had nothing to do with Trump threatening back in August that Zuckerberg would “spend the rest of his life in prison" if he did "anything illegal" to influence the presidential election. Following the Republican win, Zuckerberg heartily congratulated Trump. And last week Meta also announced a new head of its global policy team’s lead, Joel Kaplan, who was White House Deputy Chief of Staff under George W. Bush. The US President-elect promptly stated that Meta “had come a long way.”

It’s part of a broader pattern that deserves attention.

For one, Big Tech has been quick to bend the knee to the incoming US president. It’s an overt form of corporate risk management. Terrified of escalating existing tensions and getting on the wrong side, major tech firms have increased their donations. It is a marked shift from their previous stance of relative political independence. None of them wants to be the focal point of a government investigation.

Next, the potential gains are substantial. As vassals to the US administration, tech firms stand to improve their global competitive position. Tencent, the largest game maker in the world, which generated an estimated $37 billion in gaming revenue globally in 2024, was recently blacklisted by the US Department of Defense. Tencent believes it was added in error as its stock price dropped 10% on the news.

It echoes the more overt protectionist policies in China that require foreign game publishers to partner with domestic firms to access its consumer market. Trump is also calling on the Supreme Court to block the January 19th deadline that would force Chinese social media firm ByteDance to sell its popular subsidiary TikTok or face a ban in the United States. Being on the right side of the incoming president has become a priority for tech companies, many of which have contributed to Trump’s record-breaking inaugural donation fund. That’s what we’re going with: donation fund.

Finally, after first promising import tariffs that are likely to disproportionally impact interactive entertainment, creative studios active in the US now also face a more treacherous domestic market. The sweeping conservatism that is about to take office is likely going to regard video games with renewed suspicion.

In November last year, now BFF to the President-elect, Elon Musk, fenced with the idea of buying Hasbro. He did not agree with the most recent updates to the Dungeons & Dragons players’ handbook, among other things, calling for the toymaker and its subsidiary, Wizards, to “burn in hell.” A week later Musk further offered to “make games great again.”

It is unclear if Mr. Musk is going to follow through on these initiatives. His outbursts against, well, everything, distract from the fact that all major platform holders are eagerly conforming to the tastes of the new administration. A generation ago large retailers like Walmart and Target removed games from their physical shelves. Given how quickly large tech firms have conceded, there’s no reason to assume digital platforms will put themselves at risk over a game.

Platform holders are the largest gatekeepers in interactive entertainment, and their politics have just shifted to meet a new cultural moment. It changes the board for developers and players alike.

Erratum

Speaking of fact-checking, I made a mistake in a recent analysis when I compared The Game Awards to the Super Bowl and the World Series. The reported 154 million viewer metric for The Game Awards represents total reach across platforms, which differs from the average audience for every minute of the Super Bowl and the average audience for the entire event for the World Series. It is a meaningless comparison, and I should have scrutinized it more closely before publishing.

The ‘apples to oranges’ comparison, while significant, does not materially impact the core analysis that The Game Awards offers an innovative platform strategy or its successful transformation of industry events into multi-sided markets connecting publishers, digital storefronts, and audiences. The fundamental thesis about business model innovation—particularly its ability to monetize attention through premium marketing inventory while maintaining platform independence—remains sound.

As such, I’ve removed the comparison from the original analysis and updated the visual. I apologize for any confusion. And, now that we’re at the start of a brand new year, I will provide more detail and sourcing for any data I use in my write-ups starting with this one.

NEWS

Call of Duty’s $700,000,000 budget

Stephen Totilo got his first scoop of 2025, observing the $700 million budget cost for a few older Call of Duty titles. Well done! It reinvigorated the conversation around the cost of making games and how it’s become unsustainable.

Along those lines, the New York Times ran an article arguing that video games “can’t afford to look this good,” because younger generations care less about spectacle. Indeed, the cost of making games has seemingly reached new levels of spending. And the Financial Times ran a piece on the upcoming GTA6 release, reciting rumors that the game’s total cost sits around $2 billion. It’s unclear if that includes the marketing and live services budget for the first few years (probably). But it puts into context why there have been so many layoffs once the cost of capital declined and demand softened.

One important note is here to make the proper distinction between game development and its marketing. Yes, AAA titles cost a lot to make. But marketing them is historically just as costly and, more recently, more expensive. It’s part of the reason why firms are increasingly focused on advancing their distribution strategies. Budgets used to be split roughly equally, but now that most of the industry is digital (see below), a cacophony of content compels creatives to increase spending to connect with consumers.

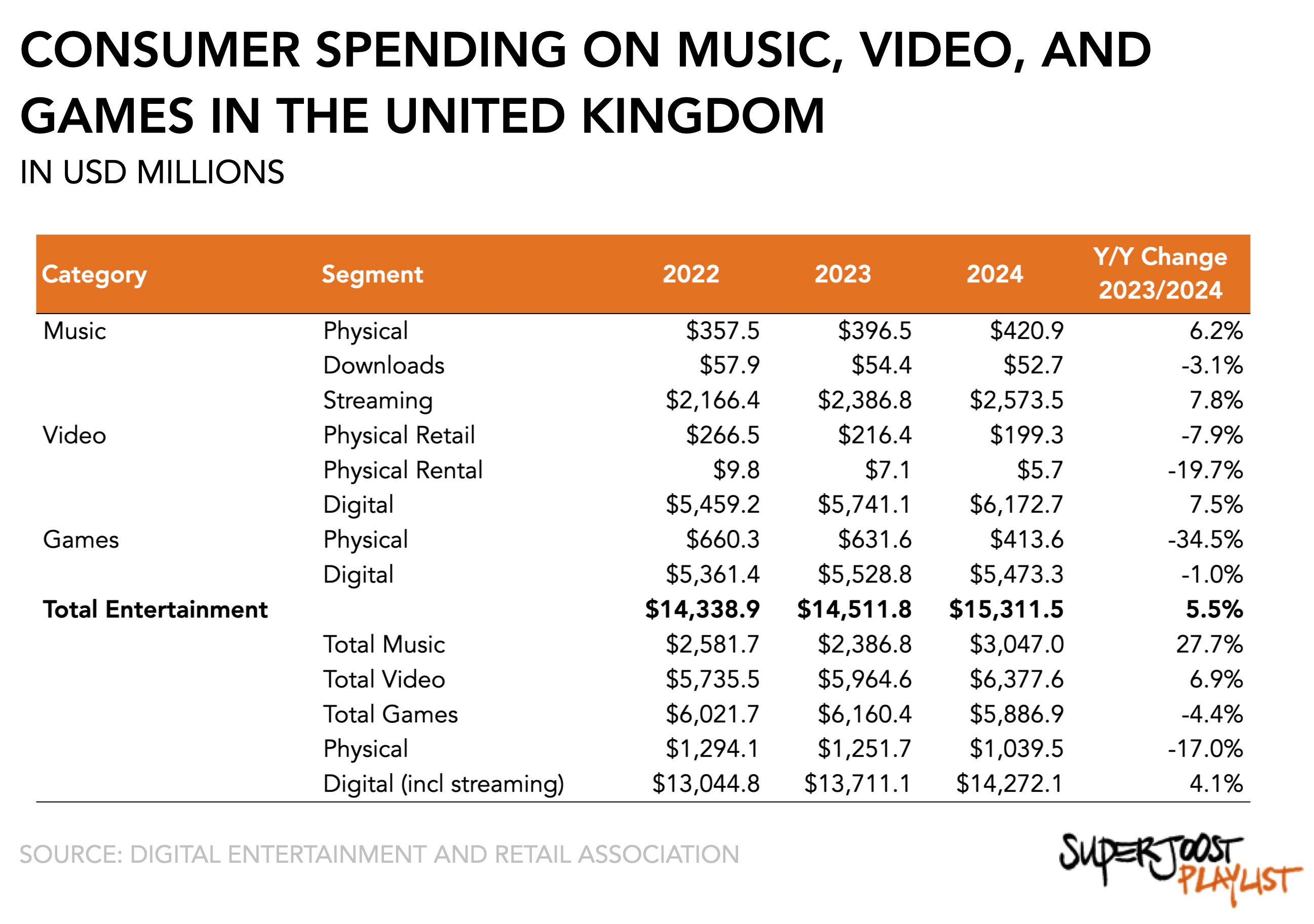

Boxed game sales down 35% in UK

A report from the Digital Entertainment and Retail Association, ERA, in the United Kingdom shows the shifting economics in music, video, and games. It’s also a great example of mental inertia among entertainment executives who cling to existing practices as the market changes.

Totaling $15.3 billion in consumer spending in 2024, up 2% year over year, the category is, however, clearly in transition.

Music reached a 20-year peak, largely attributed to the parallel growth of streaming and vinyl formats. According to the ERA, total recorded music revenues were up 7% to $3.05 billion, exceeding the previous record set during the CD era. The growth reflects the evolution in consumer behavior, with streaming revenue rising 8% to $2.6 billion while vinyl sales growing 11% to $250 million. This, I imagine, is largely the result of UK hipsters preferring to listen to low-grade audio while crafting and brewing beer in their bathtubs. Maybe. I’m not sure it deserves to be in the headline.

Video maintained its position as the largest entertainment segment among the three, with revenues climbing 7% to reach $6.4 billion, driven primarily by subscription-based streaming services. Streaming video and related digital services now account for nearly 90% of revenue with $4.5 billion from subscriptions alone.

Finally, the gaming sector’s 4% decline to $5.9 billion in 2024 is in line with the broader global trend. Physical game sales were down 35% year over year, compared to a 1% decline for digital game sales. The overall games industry is currently transitioning to a period of distribution innovation, which I’ve outlined here, and is evidenced by ERA’s reported numbers like subscription services growing 12% while traditional purchase models decline across PC (-5%) and console (-15%) segments.

As for methodology, the report synthesized data and estimates from a variety of metric providers, including The Official Charts company for music and video, Omdia (games rental and digital games), GSD/IFSE, and Futuresource Consulting, and Nielsen / GfK Entertainment for physical game sales. It’s a bit of a data mosaic, to be fair, but it’s what we’ve got.

The report’s chipper tone about the relevance of physical retail is understandable given ERA’s loyalties, with most of its board members hailing from music retail. But combined over all three entertainment categories, physical sales account for only 7% of total consumer spending—just over $1.0 billion out of a total of $15 billion—and is down from 17% the year before. Physical retail's diminishing relevance underscores a structural market transformation that extends beyond cyclical changes. It suggests the urgent need for traditional intermediaries to fundamentally reimagine their value proposition in an ecosystem increasingly defined by direct-to-consumer distribution models.

PLAY/PASS

Play. Sony announced a Helldivers 2 movie and an upcoming anime series based on Ghost of Tsushima.

Pass. It’s too bad so many game journalists got the boot last year. If nothing else, we’d possibly have better reporting and fewer crappy Switch 2 leaks.

UP NEXT

Once I get a handle on the deluge of 2025 predictions from a growing number of gaming pundits, I plan to provide a meta-analysis. If enough people voice their expectations, we’re bound to be 100% correct at some point.

Thanks for the ERA figures. Are those for the UK market only? I ask, because I thought gaming was vastly bigger then the other categories, but in these figures it's far from.

Eagerly looking forward for the meta-analysis.