Ubisoft and the technology trap

What a decade of VR, cloud, blockchain, and AI failed to deliver

The SuperJoost Playlist is a weekly take on gaming, tech, and entertainment by business professor and author Joost van Dreunen.

I’ll admit that spending time on the mountain, away from the noise and 96°F (36 °C) heat in Brooklyn, tends to bring out my caveman self.

Quiet mornings watching deer prance around. A big pot of coffee and a long stare into the distance. Closing the barn door after another nightly visit from the local family of black bears. Naps. A fire in the evenings. Howling at the moon.

Well, no. There’s no howling.

But the quiet does surface a host of new ideas and ambitions. I see now that to live in New York, you have to leave the city for a stretch each summer. Most of all, it forces you to relearn which noises require your attention and which are just the usual rustling of small animals or the wind.

Whatever happens on the mountain, though, I’m bringing it all back with me when I descend to the city. Prepare yourself.

On to this week’s update.

BIG READ: Ubisoft and the technology trap

Last week, Ubisoft published its 2025-26 annual report.

Mon Dieu.

The 356-page document records the worst year in the company’s four-decade history and offers telling insight into the industry’s tension between creative talent and technology.

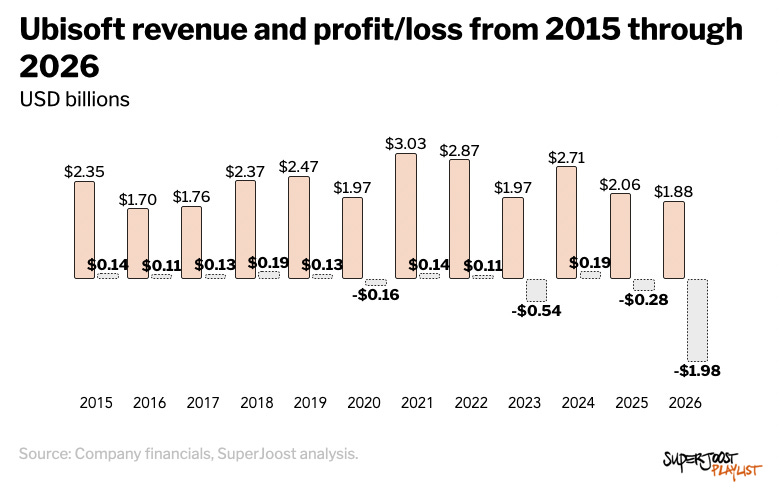

Over the past decade, Ubisoft’s revenue has sat between $1.7 to $3 billion without ever really growing. At the same time, the firm has reported only modest profits. And now, in 2026, it reports a $1.98 billion loss, larger than any profit it had booked over the entire stretch. Ubisoft just suffered a historic loss after canceling six major games under development, which forced it to close two studios and to ask Tencent to cover its debt in exchange for partial ownership of its most successful IP.

It is hardly a surprise then that CEO Yves Guillemot’s opening letter calls 2026 “a year of decisive action” and “one of the most ambitious transformations in the Company’s history.”

The question among investors is, how does Ubisoft intend to return to growth?

Naturally, the first order of business has been to cut jobs. Again.

Since 2025, Ubisoft has eliminated 1,200 positions, canceled development of six titles (including a remake of Prince of Persia: The Sands of Time), and closed two studios, all in an effort to reduce costs. At its peak in 2022, Ubisoft employed 20,665 people, a figure it has since reduced to 16,590, roughly 20 percent, according to its earnings report. So far, culling its headcount has done little to improve its share price.

A second part of Ubisoft’s answer is its apparent invigorated focus on fewer titles, smaller teams, and, ultimately, higher-quality games to return to profitability. Early indicators, including higher Metacritic scores and the recent success of Assassin’s Creed Black Flag Resynced (a remake of the 2013 release), are promising.

But the more contentious strategy is Ubisoft’s approach to “reclaim its creative leadership” by leveraging “cutting-edge technology” and "the latest innovative technologies.”

It has become a familiar executive reflex. Especially for publicly traded firms valued by investors for their future potential and growth, technology is a magical box that, once opened, will, ostensibly and at an undefined point in the future, create immense value and prosperity.

In this case, Ubisoft proposes a strategic plan that focuses on leveraging

“AI at scale to enhance creativity, improve efficiency and deliver more innovative, immersive experiences”

and a pledge to become the home for “engineers shaping the future of game technology.” But, as I’ll show, this is hardly a change from its strategy over the past decade, and so far, being at the forefront of emerging tech has failed to deliver the French publisher a clear strategic benefit.

The technology trap

To be clear, technology here refers not to code or silicon, which are simply the material games are made from. Instead, it refers to the industry’s recurring conviction that the next platform, the next tool, the next acquisition of an engineering team is a strategy in itself, a way to buy the future without having to imagine it.

I’ve previously written about the game industry’s billion-dollar gamble, describing how developers tend to leverage new technological affordances not to create more efficient production processes, but expand their creative visions. Ambition expands with fancier tools, and there have been plenty of those.

The 2014 acquisition of Oculus by then-Facebook, for instance, kicked off a push into virtual reality. Billed at the time as the next big platform that would supplement, if not outright replace, existing screen-based experiences, its promise has yet to materialize. Even so, several major firms invested heavily, including Meta, Valve, Apple, and Sony.

Months before the PlayStation VR even released, Guillemot told analysts during an earnings call,

“We believe a lot in virtual reality, because we see it’s really giving a chance for gamers to be immersed in worlds. We are developing a certain number of games that are going to take advantage of these new possibilities.”

Hoping to associate itself with the new device, it developed a virtual reality experience called Eagle Flight that allowed players to experience Paris from an eagle's perspective.

Next, when Google announced its cloud gaming service, Stadia, at the 2019 Game Developer Conference, Guillemot could be spotted in the front row during Google CEO Sundar Pichai’s keynote. Ubisoft had struck a deal that would allow Google to feature Assassin’s Creed Odyssey both as a title to beta-test the service and as a foundational title in its content portfolio.

Stadia lasted three years before Google pulled the plug. But Ubisoft’s appetite for cloud outlived the platform it had lined up to endorse. In 2023, when Microsoft needed to satisfy British regulators to close its $69 billion acquisition of Activision Blizzard, it was Ubisoft that stepped forward to absorb the cloud rights Microsoft was forced to shed. It spent an estimated $100 million to obtain the rights from Microsoft to drive traffic to its own fledgling cloud service, Ubisoft+.

According to Ubisoft's annual report, those cloud streaming rights now sit on its balance sheet at a gross value of roughly $79 million, already amortized and impaired down to a net $36 million, close to half of it gone, with a further $19 million written off the goodwill on its cloud-gaming unit. It concedes that cloud gaming remains “promising in the medium term” but “progressing unevenly,” still boxed in by technical, economic, and regulatory limits. Which is the annual-report way of admitting the market never showed up.

Ok, so it took a few losses, but was there another technology that gave Ubisoft an edge? Well, Guillemot was also a strong proponent of the metaverse. Lyrical with the notion of an expansive, interconnected digital realm at the time, he called it “the industrial revolution of tomorrow” in 2021.

Doubling down on his excitement, a few months later, at the height of the crypto craze, Guillemot described decentralized digital currencies in no uncertain terms.

“This industry is changing regularly with lots of new revolutions happening. We consider blockchain is one of those revolutions. […] We think it’s going to grow the industry quite a lot. We have been working with lots of small companies going on blockchain, and we start to have a good know-how on how it can impact the industry, and we want to be one of the key players there.”

Ubisoft promptly made a string of investments, including Aleph, a cross-blockchain network focused on decentralized applications; Sorare, a global fantasy football game; Sky Mavis, known for Axie Infinity, a digital pet universe; and Animoca, a leading blockchain gaming company at the time.

By late 2025, long after the blockchain fervor evaporated, Guillemot had simply found his next revolution. During Ubisoft’s half-year results in November, he set aside a segment of the call for generative AI, which he said the company had by then embedded across all its studios, in programming, art, and overall game quality. He called it “as big a revolution for our industry as the shift to 3D,” and added, with characteristic modesty, that Ubisoft had “everything to lead on this front.”

Zelnick says no

In contrast, one of his remaining colleagues, Strauss Zelnick, the CEO of Take-Two, spent the same decade saying no.

His response to virtual reality, for example, was quite different. On a 2021 earnings call, he told investors that the buzzwords of VR “didn’t get this industry too far,” that AR and 3D had done little better, and that what actually moves the dial is “amazing creativity, great characters, great stories, great graphics, great gameplay.” This, despite Take-Two’s reputation for open worlds that looked tailor-made for an immersive interface.

The metaverse left him equally cold. While analysts expected Take-Two to be a prime candidate to build and benefit from this tech vision, Zelnick denied that it was a new category at all, arguing instead that the firm was “probably the biggest metaverse company on Earth” already, by revenue and profit, on the strength of GTA Online and Red Dead Online. He warned that when enough money gets thrown at a word, you can "probably guess how it's going to end," and the answer is usually "not well."

While he did see some merit in blockchain’s ability to verify ownership of digital goods, calling himself a “big believer,” he rejected the more speculative infrastructure that would become so central to cryptocurrency. “When a company that didn’t exist two years ago launches with a whitepaper, a blockchain-based metaverse, and sells hundreds of millions of dollars of digital real estate in a two-day period,” he said in 2022, “I’m a little skeptical.”

Finally, both Take-Two and Ubisoft suffered the same fate when Google announced its Project Genie in January. When prompted, Zelnick took a similar position, stating, “The notion that AI can make GTA is laughable.”

Tech for what

The differences in opinions and expectations regarding novel technologies are reflected in the differences in each firm’s share price today. While Ubisoft has consistently tried to be at the forefront and has been quick to invest in tech-based innovations, Take-Two has deliberately held out.

Looking at the long-term share price history of both firms, it’s tempting to conclude that Zelnick’s skepticism has served Take-Two well, whereas Guillemot’s unfounded enthusiasm for technology has done little for Ubisoft. But the divergence doesn’t start with Guillemot’s embrace of technology. It starts, years later, when the games stop landing. Chasing each of these cycles, rather than executing its releases well, is what pulled Ubisoft down.

Technology deserves to be scrutinized with the same vigor that executives use to make job cuts.

Especially when facing exogenous circumstances like the skyrocketing cost of hardware components resulting from AI hyperscalers’ aggressive investments, making job cuts the first and primary reaction may prove even more costly down the line. If we're willing to scrutinize headcount that closely, we should be just as willing to challenge our own biases about which technologies are actually instrumental to long-term success.

Talent is the games industry’s most valuable resource and, reliably, the first to be cut whenever it comes time to improve margins or overhaul an organization. People are among the most expensive line items in game development, and they are far easier to lay off than a failing technology bet is to unwind. A wrong call on a platform or an engine, made years earlier, can quietly prove more costly, even existential, than any salary, yet it almost never draws the same scrutiny. Rather than tying its fortunes to the next wave, Ubisoft and firms like it would be more likely to benefit from focusing on what it already does well: making games.

There are obviously other factors in either firm’s trajectory. But in a market where the cost of hardware and software has skyrocketed, it’s worth remembering that some of the most enduring games we have came out of technical limitation, not abundance. Play existed long before silicon. As we head into earnings season, expect no shortage of speculation about where interactive entertainment goes next.

Just watch how much of it is about the tools, and how little is about the games.

NEXT UP

Starting August 6th, I’m raising the price of the monthly paid subscription. The reason is two-fold: it will allow me to (1) pay for someone to help with the heavy lifting on the data and analysis, and (2) increase my publishing frequency. Anyone signing up for the annual plan before August 6th will pay the current, lower rate for another full year.

That exec quotes vs. stock price chart is an all-timer. Just brutal.