Layoffs by design

How company ownership drives layoffs in the video game industry

The SuperJoost Playlist is a weekly take on gaming, tech, and entertainment by business professor and author Joost van Dreunen.

As Roblox continues to expand in its reach and relevance, two things are happening.

The first is, of course, that we are witnessing the emergence of a novel channel that facilitates some innovative new forms of play. If you haven’t already, you should check out Grow a Garden. These breakout successes are generating their own subset of teenage millionaires, which is cultivating a new generation of digital creatives.

Roblox’s immediate response to these homebrew successes has been to publicize them, of course, as indicators of cultural relevance and creative activity. Its positioning as a digital playground is starting to manifest and, from the looks of it, quite lucratively so.

Second, Roblox will likely encounter growing pushback. Such is the nature of success. I provided some feedback and comments to this week’s write-up on After Babel, the substack started by my NYU colleague, Jonathan Haidt. I’ve previously reviewed his book, The Anxious Generation, and was happy to help guide the conversation in a more equitable direction. It’s well worth the read.

The same platform that empowers new forms of play also invites new forms of pressure. Even digitally, you reap what you sow.

On to this week’s update.

BIG READ: Layoffs by design

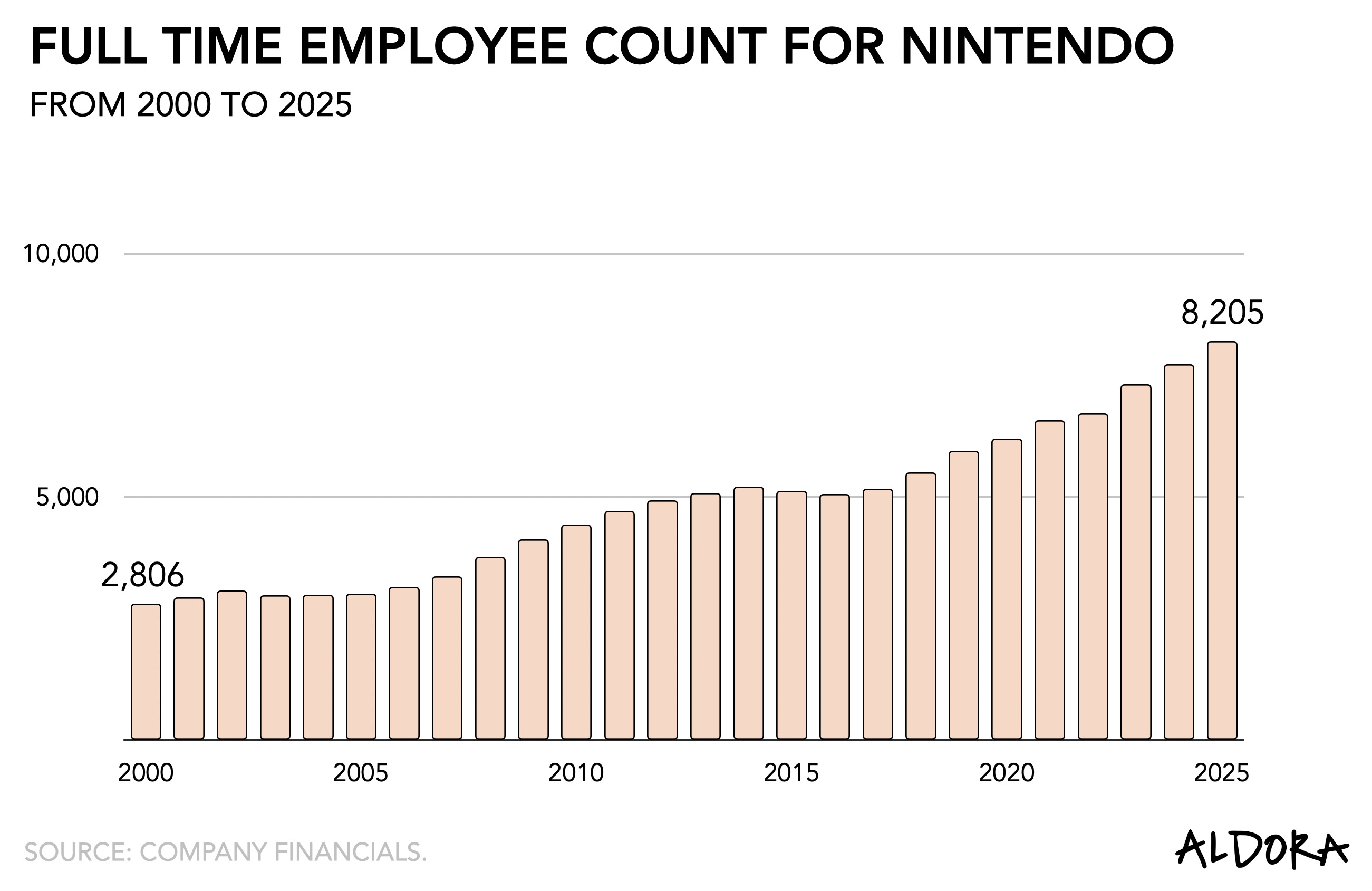

In yet another year defined by job losses, Nintendo is hiring.

According to its latest financial filing, the Kyoto-based company grew its staff size by 6%—from 7,724 to 8,205—reaching an all-time high. Even more notable is its attrition rate, which remains under 2%. At a time when “efficiency” is the industry’s favorite euphemism for cost-cutting, Nintendo’s growth seems almost contrarian.

But it is not alone.

The shift is not industry-wide. While public firms are contracting, in Europe, privately held studios are bucking the trend.

What follows is the final installment of a three-part analysis of the industry’s ongoing labor reset.