Epic decline

Judge the might of an empire by its champions

The SuperJoost Playlist is a weekly take on gaming, tech, and entertainment by business professor and author Joost van Dreunen.

It’s in the nature of empires to destroy themselves.

But instead of a sudden collapse, the root cause is often a gradual loss of control of the very systems that made them dominant in the first place.

The news of Epic Games’ latest layoffs adds to the mounting evidence of the real-time collapse of American cultural dominance in interactive entertainment. After decades of setting the tone for video games, US-based game makers face a bevy of strategic and economic challenges, forcing them to adapt to a new world order.

We can observe the signs of this decline when even the largest, most innovative, and most successful entertainment firms begin to struggle. As I see it, Epic Games is more than a casualty of bad timing or a bad quarter. It is the most legible example yet of what happens when structural conditions make decline inevitable.

Last week, it became painfully clear that, at long last, Fortnite’s cultural moment is starting to fade. Its active user count has been more or less stagnant for several years, in contrast to rivals like Roblox, which have grown. Even the investments and collaborations with Disney and LEGO have not led to sustained growth in the user base. And despite a well-executed strategy around the use of licensed IP (e.g., Star Wars, Marvel), its product market fit is waning.

Certainly, using someone else’s IP imposes a ceiling on creativity. You can play as Darth Vader, but you can’t make him your favorite color, give him wings, or bend him to your own aesthetic expression. In the absence of organic growth, Epic Games has spent a lot of time playing defense, ultimately leading to the firing of 1,000 employees.

As Bloomberg’s Jason Schreier observed, these layoffs are a symptom of more deep-seated problems. Companies spent the last decade chasing the live-service model that Fortnite pioneered, wasting billions in the process, he writes. The cruel irony is that even one of the OG free-to-play titles is proving unable to sustain itself.

Forever games, it turns out, aren’t.

By comparison, Roblox, for all its brainrot chaos, lets players create culture rather than consume it. Instead of playing in a world designed and shaped by incumbents, the comparatively unstructured playspace Roblox offers allows for greater expressive variety. There’s a reason why those Brainrot games are so jarring to your sensibilities. They are not for you.

But Schreier doesn’t take it far enough. Beyond the surface-level, Epic Games’ decline points to a cascade of market developments.

One major contributor now showing its true impact is the encroaching, disproportionate power wielded by platform holders. Over the ten years leading up to 2025, platform revenue, from app stores, console marketplaces, and digital storefronts, jumped from $14 billion to $41 billion, a 191 percent increase. By comparison, game publishers saw their revenue rise from $65 billion to $128 billion, a more modest 98 percent increase. Over the course of a decade, gatekeepers have captured value at nearly twice the rate of content creators.

In the United States, we now see what happens when platform holders gain disproportionate power in interactive entertainment. Unlike legacy platforms (ie, console makers), firms like Apple and Google don’t make games themselves and have little interest in cultivating a healthy ecosystem beyond their ability to extract revenue from it. A key example is Roblox, which is still financially vulnerable despite its massive success. Even with nearly 150 million daily active users, Roblox remains unprofitable. Instead of allowing publishers to offer discounts and benefits to their most avid players, platform firms have insisted on keeping as much economic activity as possible within the confines of their walled gardens.

After taking both Apple and Google to court, Epic Games is now licking its wounds. The cost of having taken on the firms at the top of the food chain is starting to materialize. Despite winning several important concessions, it has spent a fortune on lawyers and forfeited even more in lost opportunities. Before its removal from the App Store, Fortnite was generating an estimated $1-$2 million per day on iOS, or roughly $500 million annually. Even after Apple’s 30 percent cut, that’s $375 million in net revenue, every year, gone. Five years later, that totals close to $2 billion.

Some would go as far as to call it a Pyrrhic victory, a battle won at such great expense that it eventually means losing the war. Maybe. But given the enormous difficulty, even the most well-capitalized challengers cannot sustain prolonged conflict with platform incumbents economically.

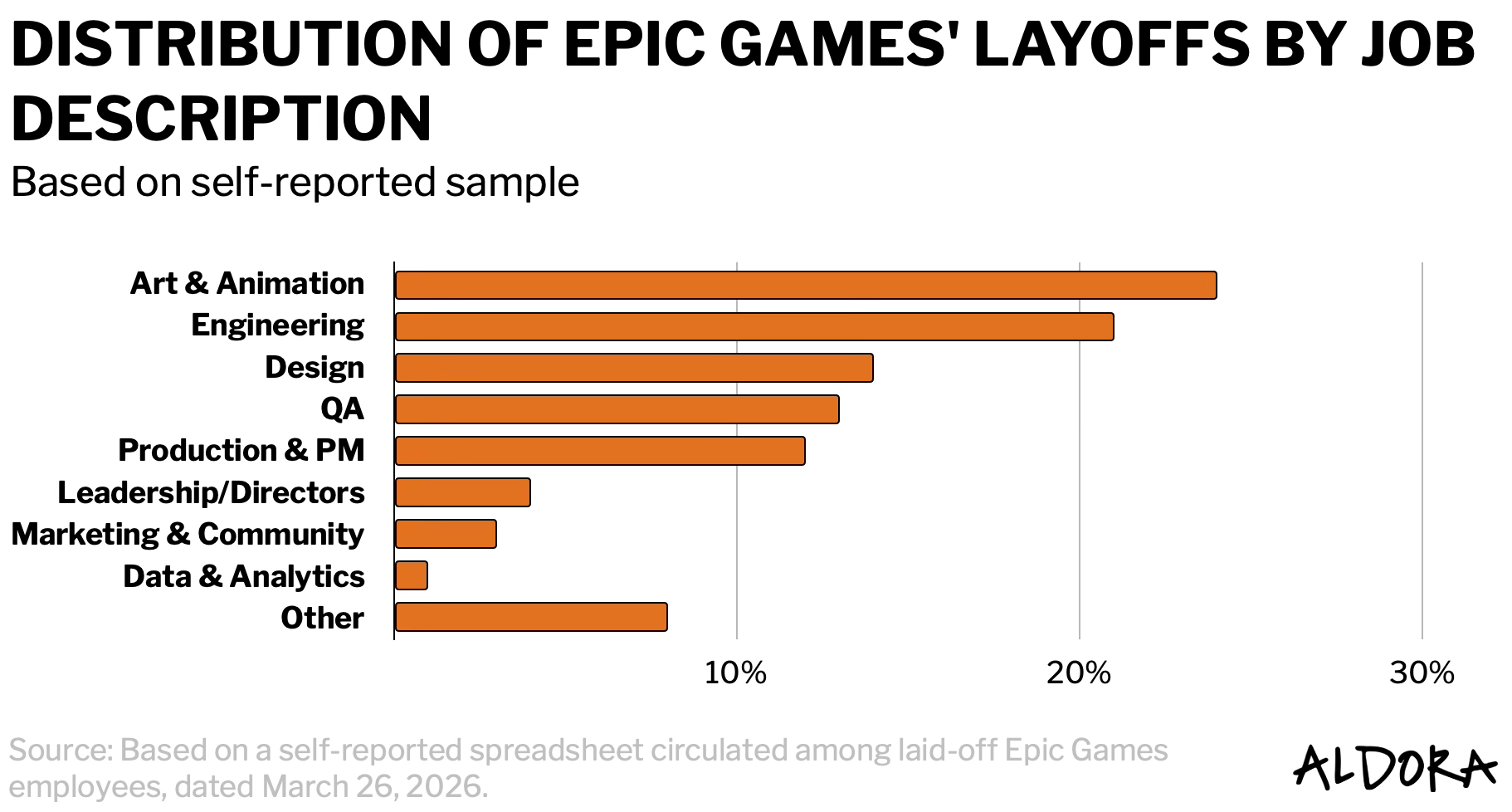

A look at the responsibilities held by those laid off makes the damage more tangible.

Based on a self-reported sample of 227 employees of the 1,000 that were just laid off, nearly half worked in art, animation, and design—the disciplines most responsible for what Fortnite looks and feels like. It suggests an incredible loss.

Further adding to the brain drain, most were also senior- and lead-level employees (the dataset shows a 20-to-1 ratio of senior to junior staff). And many of the people who lost their jobs worked directly on LEGO Fortnite, one of Epic’s most significant strategic bets. It is hard not to read this as a creative bloodletting that cuts into the company’s future.

Unforced errors

A second contributor to the erosion of American leadership is the rising cost structure of its domestic market. As demand softened, instead of lowering prices, playing video games has become more expensive. The Switch 2 launched at a 50 percent higher price point, and while it is, thus far, one of the fastest-selling devices in the firm’s history globally, the domestic picture looks quite different.

According to Bloomberg, Nintendo cut production of the Switch 2 by over 30 percent after US holiday sales fell well short of expectations. Its performance in the United States was roughly 35 percent lower than the original Switch’s during its debut, making it the worst November for hardware sales in the region since 1995. It has normalized a higher price point for everyone else, too.

According to an analysis by the Federal Reserve Bank of New York, in 2025, “nearly 90 percent of the tariff’s economic burden fell on US firms and consumers.” It’s why $1,000 consoles are now the norm. At scale, American game makers navigate higher prices, lower flexibility, and a structurally less competitive domestic market.

And speaking of self-inflicted injury, adding a $100,000 fee to H-1B visa applications virtually ensures that publishers will relocate talent elsewhere. It makes the US less competitive and causes it to miss out on tax revenue from high-earning employees.

The ravenous appetite for hardware components is similarly making games more expensive. Never mind that NVIDIA has largely pulled away from interactive entertainment now that it has found trillion-dollar success in catering to AI hyperscalers. But high-end components (e.g., RTX 5090) have become prohibitively expensive even for the more affluent PC builders.

Taken together, these are not isolated pressures but compounding constraints on production, talent, and consumption.

The sun comes up in the East

At the same time that American preeminence is starting to flicker, the lights are burning brighter everywhere else.

In Europe, a new generation of smaller, more agile firms is building audiences even in the most cluttered gaming categories. In places like Turkey and Israel, a slew of new studios has sprouted with a talent for user acquisition, even if their content doesn’t rank at the top tier of high-brow entertainment.

Scopely, for instance, recently valued the 8-month-old studio Loom Games at close to a $1 billion when it took a majority share. And last week, Nazara, a Mumbai-based gaming and esports firm, invested $100 million in Bluetile, a studio in Barcelona that specializes in social and casual games.

An important part here is the difference in DNA. Many firms that succeed in current market conditions do so by embracing novel technologies. Western developers and audiences insist that they disdain generative AI.

When Sandfall, the maker of Clair Obscur: Expedition 33, admitted to using AI to generate a handful of placeholder textures during production, a grassroots awards body promptly stripped its Game of the Year win. Never mind that every major ceremony (e.g., The Game Awards, the Golden Joysticks) kept their honors. The backlash says less about the creatives and more about an industry culture that has decided purity matters more than pragmatism.

show early gains followed by decline. European firms (CD Projekt, Ubisoft, Paradox, Stillfront, Embracer peers) exhibit higher volatility with a downward trend. Asian firms (Nintendo, NetEase, Nexon, Capcom, Square Enix, Bandai Namco, Sea) demonstrate stronger and more sustained growth before a recent pullback.")

Meanwhile, the games industry that has emerged in China, India, and Southeast Asia is part of a broader internet-based industry. It presents a generation of creative firms that is more inclined to embrace technologies like AI, which, especially in cluttered markets, enables them to scale and succeed. Moreover, in these regions, publicly traded game makers in Europe (+60%) and Asia (+26%) have, on average, performed notably better than their American counterparts (+18%) in 2025.

As for Epic itself, Tim Sweeney is a builder, not a suit. He took real technological and regulatory risks because he genuinely believes in a better future for games, and my bet is he navigates this the way he has every previous crisis.

The assumption that American game makers would indefinitely set the terms of global interactive entertainment—culturally, commercially, technologically—is no longer operative. The platforms they built on have turned against them. The audiences they cultivated are moving on. And the competitors they ignored are now eating their lunch.

Empires don’t collapse all at once. They hollow out, slowly, until one day the walls come down and everyone acts surprised. We are currently somewhere in the middle of that process.

I worked on a game with Infinite in the title once. It was a forced inclusion by execs. The original name I had proposed even focus tested much better. Any creative thing or pursuit that includes words like "infinite" and "forever" or similar words isn't likely to be that. Change is human and inevitable.

Roblox is technically highly profitable. They just spread revenue from robux over 27 months. Also invests a lot back into business. They can limit reinvestment and be $1b up if they want to.

Their developer model payouts is not that great. Devs give up around 50-75% of profits to platform + are paid in virtual currency of which fx they don’t control.

I can see it being disrupted by Epic (or a big Chinese game).