Unbundling Xbox

"The acquisition strategy didn't work."

This week’s announcement that Xbox is cutting roughly 3,200 jobs and divesting five studios marks the most significant restructuring in the division’s history.

It is also an admission that its decade-long campaign of buying up studios and intellectual properties did not yield the desired result. After spending close to $80 billion, Xbox struggles to produce the hits needed to drive adoption of its Game Pass service and fails to capitalize on its existing portfolio of proven IPs.

Following a charm offensive by recently appointed CEO Asha Sharma during her first 100 days, the honeymoon phase is clearly over.

After building up some initial goodwill and silencing critics skeptical of her lack of gamer credentials, she announced layoffs and divestitures as part of her effort to address Xbox’s troubles. The games division struggles internally with a bloated structure and a lack of quality control as it confronts what Sharma calls the “most severe hardware crisis in the industry’s history.”

Sharma’s decision to aggressively reduce Xbox’s overhead, totaling 20 percent overall, is a direct response to the shopping spree by its previous CEO, Phil Spencer. In an attempt to grow Game Pass’ subscribership, Spencer rapidly expanded Xbox’s operations, but that effort ultimately failed to deliver.

Instead, Microsoft’s gaming division has grown into an unwieldy organization, leaving some sobering conclusions for Xbox in particular and the industry in general. Or, as one person close to the matter told me,

“The acquisition strategy didn’t work.”

What we’re witnessing is a broader market correction. After a decade spent chasing scale through acquisitions, the games industry is shifting back toward distribution, where efficiency, reach, and organizational discipline matter more than the size of your portfolio.

I’ll review what went wrong, what the next steps could look like, and what it says about the industry at large.

The Great Unbundling of Xbox

An apparent lack of financial discipline among many of the studios it acquired over the past decade is a first point of failure.

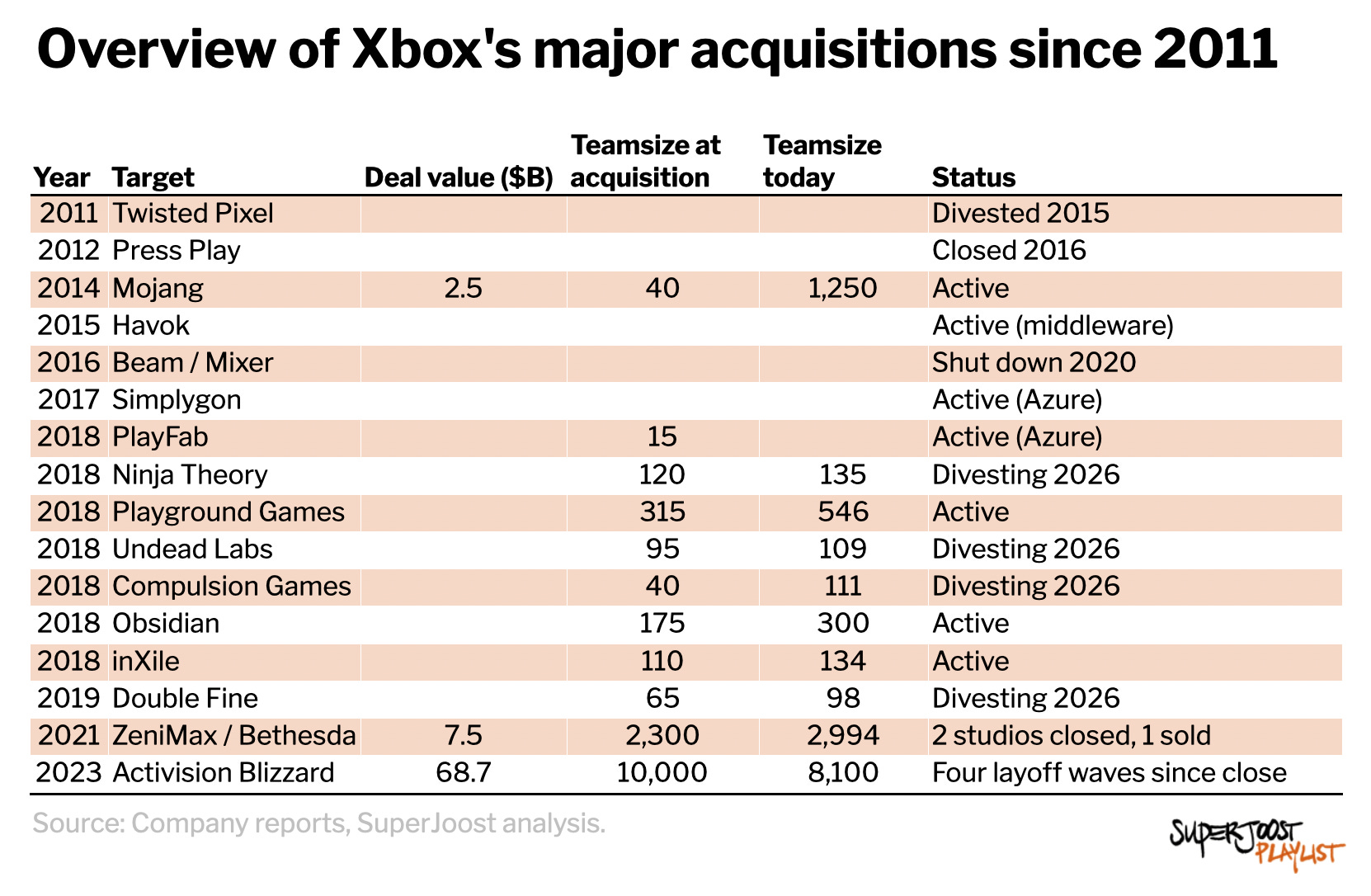

Under its previous CEO, Phil Spencer, Xbox more than tripled in size through a sustained, ambitious acquisition strategy. Since 2011, it has made 16 acquisitions, escalating in size and ranging from middleware to indie studios to publishers.

As Xbox is repositioned from a growth engine to a value-creation engine, studios will be held to a different financial standard. Given the early signaling we’ve seen so far, I’d wager that many, if not most, of Xbox’s current studios aren’t financially self-sustaining.

Sharma all but confirms it, conceding that in a typical year, Xbox “lost 64 cents for every dollar we invested,” and that it is “not the best home for every type of studio.”

Former Xbox executive Laura Fryer, in a recent video dissecting the division’s troubles, arrived at the same diagnosis. Once the priority shifted back toward profitability, she notes, "a lot of those projects couldn't stand on their own."

It’s common practice, of course, especially in the culture industries, to subsidize creative projects with funds from more successful ventures. Media execs often mistakenly pursue a portfolio approach, diverting resources from the titles and studios that perform well and thereby limiting their upside potential.

The demonstrably stronger strategy is doubling down on your winners, which is the only road to breakout success. A balanced portfolio, in contrast, produces precisely the kind of underperforming releases we’ve seen from Xbox more recently.

Expanding its first-party portfolio as dramatically as Xbox has compounded the problem. Its share of publishing revenue from owned titles jumped from 28 percent before the Activision Blizzard deal to 61 percent after.

Its rival Sony has pushed in the opposite direction, relying on only 29 percent of its own IP and the rest on third-party content. Platform holders do this because it offloads risk to external developers, while still maintaining centralized control over their content rollout.

Sony has spent the past decade leaning into exactly this posture. Its third-party publishing revenue nearly doubled to around $11 billion over the decade ending in 2025, even as Xbox, by folding in Activision Blizzard, deepened its dependence on its own catalog. Sony’s executives meet regularly with the major publishers, giving them visibility into product roadmaps nearly a decade out—knowledge they use to shape release timing, shelf space, and distribution leverage. Xbox ran the opposite play at the worst possible moment.

As part of her reset for Xbox, Sharma is pushing five studios out of the Xbox portfolio: Ninja Theory and Undead Labs are being sold, Double Fine and Compulsion are being spun out to their founders with their IP and catalogs intact, and Arkane's Lyon studio is entering consultation to be sold or spun out. Nevertheless, almost exactly 1,000 days after ABK/MSFT formally closed, we’re witnessing the Great Unbundling of Xbox’s games portfolio.

No meaningful presence in mobile gaming, still

Xbox’s mobile shortcomings are not separate from its acquisition problems. They are evidence of them.

You’ll recall that owning King Digital, maker of Candy Crush, was central to the argument Microsoft made to regulators to get the Activision Blizzard deal approved. Succinctly, mobile is the largest segment in games—bigger than PC and console combined, at roughly 61 percent of global games revenue, and it is governed by two gatekeepers, Apple and Google, who, in the CMA’s own words, “hold all the cards.”

According to a 2022 filing submitted to the UK’s Competition and Markets Authority, Xbox had “no meaningful presence in mobile gaming,” a gap the acquisition was meant to close by providing “capabilities and content on mobile, which it currently lacks, while creating new distribution options for game developers outside of mobile app stores.”

Folding in Activision Blizzard’s mobile business, roughly $3.2 billion a year at the time of the deal and anchored by Candy Crush, would make Microsoft the third-largest mobile game maker in the world, behind only Tencent and NetEase.

If it had executed well, it would have both bolstered Xbox’s share in mobile and helped counter the duopoly's grip on the market. However, almost none of it materialized. King demonstrates the central weakness of Xbox’s acquisition strategy. Buying distribution capabilities is not the same thing as building them. It requires a far more dedicated effort (something, for instance, both Activision Blizzard managed with the initial acquisition of King in 2016 and Take-Two with its purchase of Zynga). In contrast, Microsoft acquired the largest mobile publisher in the West and still failed to establish a meaningful position in mobile distribution.

What was positioned as the crown jewel of the entire regulatory case was left to coast on a decade-old puzzle game rather than being built into the beachhead. Microsoft’s plan for a dedicated mobile storefront, pledged in the same filing as "a new Xbox Mobile Platform" that would scale the Xbox Store across devices and pull players from the App Store and Google Play, has yet to materialize in any form that threatens the duopoly.

That’s a big promise to leave empty.

Sharma’s goal of one billion daily active users reemphasizes the importance of mobile. There is no arithmetic that reaches a billion through console and PC alone—especially not with a franchise slate that skews older and console-bound, and resonates only poorly with Gen Z and Alpha players who live on mobile. That is why she is now pulling King and Mojang out of the studio pool to report directly to her, singling them out as Xbox’s largest properties by monthly active players and its best source of geographic and demographic reach.

Xbox’s failure to execute leaves an existential gap. In Microsoft’s own words to the CMA, it remained “nowhere in mobile game distribution globally.” If I had to guess, mobile was also culturally the most different, and instead of pulling it closer, management let it drift.

The thousand-dollar box

A third point of failure is Xbox's exposure to the hardware crisis.

Start with the price of the box. For the industry’s entire history, console hardware has followed one iron rule: it gets cheaper over time. Makers sell at or below cost at launch, then ride components downward. On average, the cost of a console drops by a third within four years, and eventually lands at about 35 percent of its original retail price by year ten.

That institutional logic is no more.

I’ve previously argued that AI is making everything more expensive, and even its rivals, like Nintendo, are competing directly with hyperscalers for component parts. Similarly, Xbox expects to pay five times as much for memory and storage in 2027 as it did in 2024. It means that five years in, the PlayStation 5 and Xbox Series X|S cost more than at launch. Microsoft charges about 19 percent more for its current console generation, and Sony about 12 percent.

Such exogenous shocks hit everyone, including Sony and Nintendo. The question worth asking is why they seemingly hit Xbox the hardest.

The answer, by Sharma’s own account, isn’t the market.

Xbox entered this console generation with a smaller install base and a higher cost structure, but bet on Game Pass and a sprawling content portfolio to close the gap. When those bets didn’t grow fast enough, it responded by adding more. More teams, more investment, more time, all “hoping for a better outcome.” That is the opposite of discipline. It is what an organization does when no one is willing to make the hard call.

And the bloat is quantified, again by Xbox itself.

Work in some parts of the company passes through as many as fourteen layers of management. Platform teams are 40 percent larger than at the start of the generation, even as players and playtime have declined. Sharma’s remedy, to cut to no more than five layers, halve vendor spend, on the logic that “great technology gets better when it gets simpler, not bigger,” is really an admission of how heavy the thing had become.

It’s a classic flaw and part of a pattern we’ve seen in the industry before. The names change, but the pattern doesn’t.

In the early 1980s, Atari expanded so quickly on the back of the home console boom that it lost complete control over what it shipped. Overestimating demand and having lost its grip on quality control, Atari mistakenly flooded the market with too many copies of its now infamous E.T.

Similarly, Hasbro’s initial success in interactive entertainment in the late 1990s encouraged executives to dream of a billion-dollar games division. The toymaker went on an acquisition spree, purchasing licenses and studios to expand as broadly as possible. Instead of being a success, it became a managerial nightmare, with independently run divisions lacking a clear financial reporting structure. In the absence of financial discipline, margins dropped, exposing the entire operation, which came undone once the dotcom bubble burst.

And, most recently, Swedish conglomerate Embracer had to walk back its pandemic-fueled ambition to become Europe’s gaming powerhouse. Financed with cheap capital, it assembled hundreds of studios, but soon would prove unable to integrate any of it. When the market turned, every studio had to service the mothership’s debt, creating a distraction from the creative work and resulting in a slow destruction of talent and goodwill. The empire broke itself into three pieces.

This pattern of a frenzied growth cycle followed by a sudden market correction that exposes especially the largest firms repeats itself. Xbox’s aggressive expansion now crashes headfirst into the financial challenge posed by the AI boom, exposing its cumbersome organizational structure to a dramatic shift in market circumstances.

The precedent

With Xbox having concluded its prelude focused on margins and started its divestitures, the more useful question is what the precedent suggests for the studios now being spun off.

Embracer’s recent history offers encouraging evidence that unencumbering creative groups can help them soar. After initially buying up gaming studios and insisting on a similar laissez-faire approach across its organization, the Swedish conglomerate eventually found itself running out of capital once the market lost its pandemic-fueled momentum.

Unable to maintain its strategic course, it began selling off subsidiaries and, in two cases, handing businesses back to the people who ran them.

In early 2024, Embracer sold Gearbox Entertainment to Take-Two Interactive for $460 million in stock and divested the core of Saber Interactive to Beacon Interactive for $247 million. In November that year, it agreed to sell mobile studio Easybrain to Tencent-owned Miniclip for $1.2 billion in cash, a deal that, on its own, all but erased the group’s net debt, which stood at roughly $1.2 billion before the sale and about $45 million after. And in November 2025, it offloaded publisher Arc Games and Cryptic Studios (Star Trek Online, Neverwinter) to Project Golden Arc, a management-led entity backed by Hong Kong’s XD Inc., for about $30 million.

Regaining their independence and living outside of a cumbersome corporate entity can oxygenate a creative vision. In a recent interview with The Game Business, Saber Interactive’s Chief Creative Officer reflected on the publisher’s newfound creative freedom, saying, “We can just do AAA titles better,” referring to the success of Warhammer 40,000: Space Marine 2, among others.

Cut loose from the mothership and handed back its own direction, a studio did better work, not worse. It is precisely the bet Sharma is making on Double Fine and Compulsion, spun out to their founders with their catalogs and runway intact.

The main event for Embracer, however, was its transformation into three standalone public entities. Initially announced in April 2024, the largest asset, Asmodee, began trading in February 2025, followed by Coffee Stain in December that year.

Here, too, consolidation was supposed to buy economies of scale, but instead, the combined revenue of the three separate entities is essentially flat compared with the old whole. Scale never materialized.

Freed to trade on its own, Asmodee’s enterprise value (~$2.9bn) today is roughly equal to what the entire pre-split Embracer was (~$3.05bn). The board game maker has been aggressively expanding, and recently reported “the strongest sales and profit performance” in its history. It tells you that the market had been pricing one strong business plus everything else at close to zero.

Built for a different era

The changes at Xbox are both painful and predictable.

In fact, they are precisely what we should expect during a shift from a content cycle to a distribution cycle. Historically, periods of consolidation and acquisition eventually give way to periods defined by efficiency, simplification, and new forms of distribution. Atari learned this lesson. Hasbro learned it. Embracer learned it. Xbox is learning it now.

The job losses are real, and they land hardest on people who did nothing wrong except join an organization that grew faster than it could govern itself. In February, I predicted this would happen.

At the time I wrote that Xbox’s new management would follow two steps. First, it would turn inward and focus on margins. Having built an empire of studios and franchises, that is what is happening now. Today’s restructuring announcement is precisely that. Second, I expected the divestitures to follow—the sell-off of assets to return the organization to health. That, too, has now arrived, almost exactly on schedule.

What I got wrong was which assets Xbox would sell. Xbox’s lackluster effort in mobile, it seemed to me at the time, would make King Digital the most sellable asset. That obviously did not happen. In fact, Sharma is bringing the mobile division closer by having King and Mojang report directly to her. It signals a course correction. A recognition that the audience Xbox needs most is the one it has been neglecting.

The unpopular opinion here is that corporate management fell short in its responsibility to maintain quality control. Had it not, Xbox’s circumstances would look different today.

Xbox’s acquisition strategy failed because it was built for a different era. The industry moved from scale to efficiency, from consolidation to distribution, and from content abundance to audience access. Xbox simply arrived at that realization later than it should have.

At first, organizations fail slowly. Then all at once.